Explore Overview

Guides Overview

Australian Health System

(25 articles)

Health Insurance Prices

(20 articles)

Private Health Insurance

(34 articles)

Private Health Insurers

(15 articles)

Medicare

(28 articles)

Medicare Benefits Schedule (MBS)

(6 articles)

Pharmaceutical Benefits Scheme (PBS)

(8 articles)

Public Hospitals

(6 articles)

Private Hospitals

(7 articles)

Medicare Levy

(7 articles)

Private Health Insurance Rebate

(7 articles)

Age-based Discount

(5 articles)

Lifetime Health Cover Loading

(11 articles)

Insurers Overview

AAMI Health Insurance

AAMI Health Insurance

ACA Health

ACA Health

ahm

ahm

AIA Health Insurance

AIA Health Insurance

Allianz Care Australia

Allianz Care Australia

APIA Health Insurance

APIA Health Insurance

Astute Simplicity Health

Astute Simplicity Health

Australian Unity

Australian Unity

Bupa Health Insurance

Bupa Health Insurance

CBHS Corporate

CBHS Corporate

CBHS Health

CBHS Health

CBHS International Health

CBHS International Health

Defence Health

Defence Health

Doctors’ Health

Doctors’ Health

Emergency Services Health

Emergency Services Health

Frank

Frank

GMHBA

GMHBA

GU Health

GU Health

HBF

HBF

HCF

HCF

HCi

HCi

Health Partners

Health Partners

HIF

HIF

Hunter Health Insurance (by CDH Benefits Fund)

Hunter Health Insurance (by CDH Benefits Fund)

ING Health Insurance

ING Health Insurance

Latrobe Health Services

Latrobe Health Services

Medibank

Medibank

Mildura Health Fund

Mildura Health Fund

Navy Health

Navy Health

nib

nib

Nurses & Midwives Health

Nurses & Midwives Health

onemedifund

onemedifund

Peoplecare

Peoplecare

Phoenix Health Fund

Phoenix Health Fund

Police Health

Police Health

Priceline Health Insurance

Priceline Health Insurance

Qantas Insurance

Qantas Insurance

Queensland Country Health Fund

Queensland Country Health Fund

Real Health Insurance

Real Health Insurance

Reserve Bank Health Society (RBHS)

Reserve Bank Health Society (RBHS)

RT Health

RT Health

see-u by HBF

see-u by HBF

Seniors Health Insurance

Seniors Health Insurance

St Lukes Health

St Lukes Health

Suncorp Health Insurance

Suncorp Health Insurance

Teachers Health

Teachers Health

Territory Health Fund

Territory Health Fund

Transport Health

Transport Health

TUH

TUH

UniHealth

UniHealth

Union Health

Union Health

Westfund

Westfund

AAMI Health Insurance

ACA Health

ahm

AIA Health Insurance

Allianz Care Australia

APIA Health Insurance

Astute Simplicity Health

Australian Unity

Bupa Health Insurance

CBHS Corporate

CBHS Health

Defence Health

Emergency Services Health

Frank

GU Health

HBF

HCi

HIF

Hunter Health Insurance (by CDH Benefits Fund)

Mildura Health Fund

Navy Health

nib

Nurses & Midwives Health

Police Health

Reserve Bank Health Society (RBHS)

see-u by HBF

St Lukes Health

Teachers Health

Transport Health

TUH

UniHealth

Westfund

News Overview

Health insurance giving Aussies less value, doctors say

Insurers paying more for hospital claims, new data shows

Aussies paying steep Gaps for specialist care, data shows

Govt warns insurers about premium increases

ACT residents paying high Gaps, as premiums set to rise

Hospital Cover claims jump 11.6% amid public hospital strain

Four times more Australians paying Medicare Levy Surcharge, data shows

Yoga, Pilates and other natural therapies return to Extras Cover

Compare Overview

Calculate Cheapest Policy

Search for a new policy based on your health cover needs and budget. We compare every insurer and every policy.

As the cost-of-living crisis continues in Australia, knowing how to save money on health insurance could pay off – literally. As experts on private health insurance, we at healthslips.com.au have plenty of great hacks for reducing the cost of private health insurance. Here’s our round-up of the best tips.

Change your excess

If you’re admitted to hospital as a private patient, an excess is the amount you’ll pay towards your Hospital Cover claim. If you increase the excess on your policy – say, from $500 to $750 – your premiums will be cheaper.

A warning: If your premium is more than $750 for a policy that covers just yourself, you won’t be exempt from paying the Medicare Levy Surcharge. If it’s a policy for you and other members of your household (such as your partner and/or kids), your excess needs to be $1,500 or less to avoid the MLS.

How do I avoid paying the Medicare Levy Surcharge?

Downgrade your cover

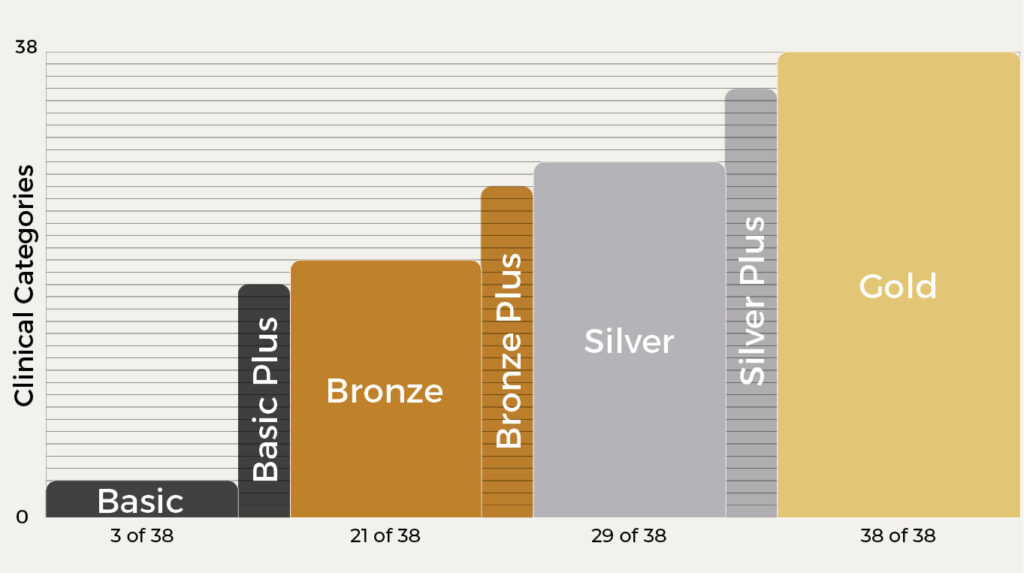

Instead of dropping their health cover, lots of Aussies are downgrading their level of cover to save money. Statistics from Private Healthcare Australia found that more than 216,000 policies were downgraded in the first half of 2024. Have a look at your policy and consider whether a lower-level policy would meet your cover needs. For example, a single adult in NSW could save $411.84 a year by switching from the cheapest Silver tier Hospital Cover to the cheapest Bronze policy.

You could do the same with your Extras policy. A single adult in Victoria pays around $181.80 a month for the most expensive Extras policy that covers everything from hearing aids to home nursing, but downgrading to one that covers only the basics (dental, physiotherapy, chiropractic and osteopathy) would mean a saving of $162 a month and $1,944 a year.

To help you choose the right level of cover, here’s a list of treatments and services on each tier of Hospital Cover, and these are the services that may be included in Extras Cover.

Consider ‘Plus’ policies

As well as Basic, Bronze, Silver and Gold tiers of Hospital Cover, many insurers also offer Basic Plus, Bronze Plus and Silver Plus policies. These can be a cheaper way to get more health cover than the standard Bronze or Silver options, without going all the way to the next tier (and price level).

Health economist Dr Rosalie Viney from the University of Technology Sydney found this when she rang her insurer about an upcoming hip replacement procedure. Her insurer told her she could save money by downgrading from Gold to Silver Plus, which still covered her hip replacement.

“It was a massive saving – about $1,200 a year,” she says. “I went very carefully through what was not covered by dropping down, and it was really worthwhile to me to go to a lower level.”

Read Dr Viney’s advice on the best age to get health insurance.

Reconsider Extras Cover

If you have both Hospital Cover and Extras Cover, ask yourself whether you really need both. Hospital Cover is the type of policy that covers your big healthcare expenses and helps you avoid the Medicare Levy Surcharge (which applies if you earn above $101,000 as a single person, or above $202,000 combined for couples, single parents and families). Since Extras Cover is for non-hospital health costs, you might decide you can afford to pay for things like dental, physiotherapy and optical services yourself, instead of having insurance cover.

Tip

Add up how much your insurer subsidised your extras healthcare expenses last year, then compare that with the amount you spent on your Extras premium. This is one factor to consider when deciding whether Extras Cover is worth having. Bear in mind, the full amount you pay for some healthcare services may be higher if you don’t have Extras Cover, since some providers have agreements with insurers to charge lower rates to members.

What’s the difference between Hospital and Extras Cover? Do I need both?

Check out corporate or restricted cover

Sometimes restricted health insurers or corporate health policies provide cheaper health insurance. Here’s how to find out if you’re eligible:

- Check with your employer whether they have any arrangements with health insurers for discounted cover. There might be information on your company’s intranet, or contact your manager or human resources department.

- If you’re a member of any clubs or organisations, such as an RSL club or gym, check whether they have arrangements with any private health insurers to offer cheaper health cover.

- If you work in the healthcare, education or emergency services field, or you’re in the military, you’re probably eligible for cover with a restricted insurer. Often these insurers also offer cover to partners or relatives with ties to these industries – for example, Doctors’ Health even offers cover to nieces and nephews of health practitioners. Check our list of restricted insurers.

Pay smarter

The way you pay for health cover could make a difference to the amount you pay. You can often get cheaper health insurance premiums by paying through:

- Direct debit

- Payroll deduction

- Advance payments – i.e. paying for a whole year of premiums. This also means you can lock in a cheaper price before the annual premium rises (which usually take effect in April each year).

Why does health insurance go up every year?

Ask your health insurer what reductions they might offer if you change the way you pay.

Look for a cheaper health insurance policy

This is really the ultimate health insurance hack. If you’ve been on the same health insurance policy for years, you’re probably missing out on a better deal. At healthslips.com.au, we leave no stone unturned, searching every single policy from every insurer on the market, showing you every option that meets your needs. It’s free and you don’t have to enter any contact details – and since we’re not selling insurance, there’s no pressure to buy. Try the healthslips.com.au Calculator and you could save money on health insurance quickly.

What to consider when choosing health insurance.

Trudie McConnochie

Writer and Researcher

Knowledge is power – that’s the guiding principle behind everything Trudie writes, and it’s a philosophy she brings to her work at healthslips.com.au. By breaking down complex information into easy-to-understand blogs and stories, she aims to empower Australians to make the best choices and an informed decision around private health insurance.

Trudie understands firsthand some of the complexity of private health insurance having moved to Australia from New Zealand and having to navigate a vastly different public healthcare system and health insurance structure.

Trudie holds a Bachelor of Communication Studies (journalism major) from the Auckland University of Technology.

Policies change monthly, stay informed

- Insurers regularly update policies, introduce new policies and close policies. Our data is updated monthly.

- We will only send information relevant to you. You can unsubscribe at any time. See our Privacy Policy.