Explore Overview

Guides Overview

Australian Health System

(25 articles)

Health Insurance Prices

(20 articles)

Private Health Insurance

(31 articles)

Private Health Insurers

(15 articles)

Medicare

(28 articles)

Medicare Benefits Schedule (MBS)

(6 articles)

Pharmaceutical Benefits Scheme (PBS)

(8 articles)

Public Hospitals

(6 articles)

Private Hospitals

(6 articles)

Medicare Levy

(7 articles)

Private Health Insurance Rebate

(7 articles)

Age-based Discount

(5 articles)

Lifetime Health Cover Loading

(11 articles)

Insurers Overview

AAMI Health Insurance

AAMI Health Insurance

ACA Health

ACA Health

ahm

ahm

AIA Health Insurance

AIA Health Insurance

Allianz Care Australia

Allianz Care Australia

APIA Health Insurance

APIA Health Insurance

Astute Simplicity Health

Astute Simplicity Health

Australian Unity

Australian Unity

Bupa Health Insurance

Bupa Health Insurance

CBHS Corporate

CBHS Corporate

CBHS Health

CBHS Health

Defence Health

Defence Health

Doctors’ Health

Doctors’ Health

Emergency Services Health

Emergency Services Health

Frank

Frank

GMHBA

GMHBA

GU Health

GU Health

HBF

HBF

HCF

HCF

HCi

HCi

Health Partners

Health Partners

HIF

HIF

Hunter Health Insurance (by CDH Benefits Fund)

Hunter Health Insurance (by CDH Benefits Fund)

ING Health Insurance

ING Health Insurance

Latrobe Health Services

Latrobe Health Services

Medibank

Medibank

Mildura Health Fund

Mildura Health Fund

Navy Health

Navy Health

nib

nib

Nurses & Midwives Health

Nurses & Midwives Health

onemedifund

onemedifund

Peoplecare

Peoplecare

Phoenix Health Fund

Phoenix Health Fund

Police Health

Police Health

Priceline Health Insurance

Priceline Health Insurance

Qantas Insurance

Qantas Insurance

Queensland Country Health Fund

Queensland Country Health Fund

Real Health Insurance

Real Health Insurance

Reserve Bank Health Society (RBHS)

Reserve Bank Health Society (RBHS)

RT Health

RT Health

see-u By HBF

see-u By HBF

Seniors Health Insurance

Seniors Health Insurance

St Lukes Health

St Lukes Health

Suncorp Health Insurance

Suncorp Health Insurance

Teachers Health

Teachers Health

Territory Health Fund

Territory Health Fund

Transport Health

Transport Health

TUH

TUH

UniHealth

UniHealth

Union Health

Union Health

Westfund

Westfund

AAMI Health Insurance

ACA Health

ahm

AIA Health Insurance

Allianz Care Australia

APIA Health Insurance

Astute Simplicity Health

Australian Unity

Bupa Health Insurance

CBHS Corporate

CBHS Health

Defence Health

Emergency Services Health

Frank

HBF

HCi

HIF

Hunter Health Insurance (by CDH Benefits Fund)

Mildura Health Fund

Navy Health

nib

Nurses & Midwives Health

Police Health

Reserve Bank Health Society (RBHS)

St Lukes Health

Teachers Health

Transport Health

TUH

UniHealth

Westfund

News Overview

Government investigates ‘price gouging’ by insurers

Health insurance costs will rise next week due to cuts in Government Rebate

Gap payments continue to rise, report finds

Cost of health insurance will rise 3.7% on 1 April

Health insurers criticised for using ‘loophole’ to raise prices

Aussies hit with higher out-of-pocket payments

Aussies warned about ‘double dipping’ by medical specialists

NSW residents may face higher bill for health cover next year

Compare Overview

Calculate Cheapest Policy

Search for a new policy based on your health cover needs and budget. We compare every insurer and every policy.

If you’re in a relationship, you might be wondering whether you can get more value from your health insurance by combining cover with your partner. Or perhaps your children have left home and moved onto their own health insurance policies, so you’re considering changing from a Family to a Couples policy. Either way, you’ll want to find the best health insurance for couples in Australia.

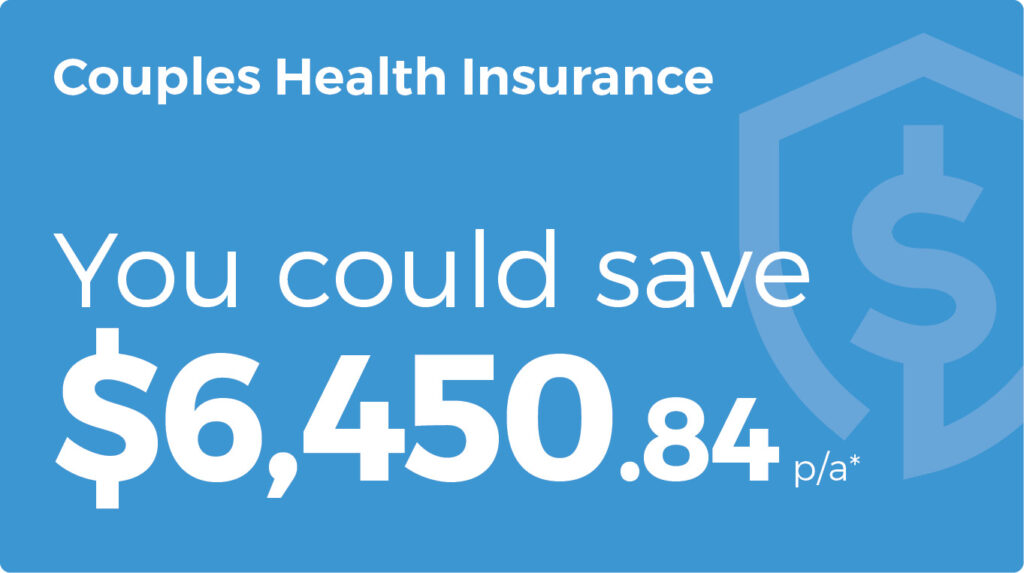

Using the healthslips.com.au Calculator to find the right Couples policy for you could really pay off – our calculations found a difference of around $6,450.84 a year between the cheapest and most expensive Silver tier Combined Hospital and Extras policies for a couple in Victoria. And with the cost of health insurance rising on 1 April, now is the time to shop around and make sure you’re getting the best deal. (Tip: you can do this easily by using our Calculator, which compares every policy in the market, and since we aren’t selling insurance, you’ll get unbiased results.)

To find the best private health insurance for couples, here’s what you need to consider.

Do I need to share health insurance with my partner?

A couples health insurance policy is a shared policy between 2 people, and you don’t have to be married to be eligible but you do need to be living together. The main advantage of a Couples health insurance policy is the convenience of paying for one policy rather than managing 2 separate policies.

You won’t typically save money on premiums with a Couples policy, but you may be able to share your benefit limits, which is helpful if one person’s need for a particular health service is greater than their partner’s, for example dental care needs.

Try the Calculator to find a good price for your health insurance needs.

Do young couples need health insurance?

If you’re a young couple, getting health insurance could be a good idea – especially if you’re planning to start a family in the near future. Hospital Cover means you’re covered for Pregnancy and Birth (if you choose the right level of cover), but there’s usually a 12-month waiting period, so you need to take out the policy before you’re ready for kids. It’s best to upgrade to a Family policy before your baby is born, to make sure they’re covered from birth.

Don’t forget about the financial benefits, either. Getting health insurance as a young couple could save you money in the future, thanks to the Age-based Discount which some insurers offer and applies to anyone aged 18 to 29 who takes out Hospital Cover. For couples, the discount is calculated as an average between the 2 of you, like in this example:

Jacob aged 26, Olivia aged 32

Jacob gets an 8% discount due to being 26 years old, but his partner Olivia is 32 and therefore ineligible. The Age-based Discount on their couples policy would be 4%, the average between 8% and 0%.

And regardless of your relationship status, taking out a policy now will also help you avoid the Lifetime Health Cover Loading, which applies to anyone taking out health insurance for the first time after age 31.

Do older couples need health insurance?

As we age, our healthcare needs increase so private health insurance can really pay off in your senior years. You and your partner could take out a policy for 2 adults where you can share your limits and manage one policy, or if you have different healthcare needs, you could get 2 single policies at different tiers, which may save you money.

What happens to the Lifetime Health Cover Loading on a couples policy?

On a policy for 2 adults, if both of you took out Hospital Cover before the age of 31 and have maintained it continually, you don’t need to pay the Lifetime Health Cover Loading (LHCL).

LHCL is calculated at an extra 2% for every year older than the age of 31 you are when taking out Hospital Cover for the first time. If one, or both, of you need to pay the Loading, here’s how it’s calculated:

- If both people in the relationship have to pay the Lifetime Health Cover Loading, the percentage will be added together. For example, Mike is 41 and his wife Bhavani is 37. Both are taking out health insurance for the first time, so Mike has 22% Loading and Bhavani has 14%. That Loading is averaged out so that their couples policy will cost them an extra 18% in Loading.

- If one person has to pay the Lifetime Health Cover Loading but the other doesn’t, the percentage of Loading is still averaged across both people. For example, if Melissa had taken out insurance at age 28 but her partner Lee didn’t get a policy until 41, his loading is 22% while Melissa’s would be 0%. Their shared policy would cost them an extra 11% in Loading (the average of 22% and 0%).

How do I find the best Couples health insurance?

To find the best private health insurance for couples, you need to take into account your age, health needs, lifestyle, family situation and income. Here are some factors to weigh up:

- What are your current health cover needs?

- Do either of you have any pre-existing health conditions?

- What is your budget?

- Is your annual combined income higher than $194,000? If so, you’ll need to get Hospital Cover with an excess of less than $1,500 to avoid paying the Medicare Levy Surcharge.

- Are you planning to start a family in the coming years?

- Is your adult family moving out of home and onto their own health insurance policy?

- Are you likely to have greater health needs in the near future?

- Do you need Extras Cover, for out-of-hospital health services such as dental, optical or physiotherapy?

- Do you need Ambulance Cover, or is ambulance treatment provided free in your state or territory? (Check here.)

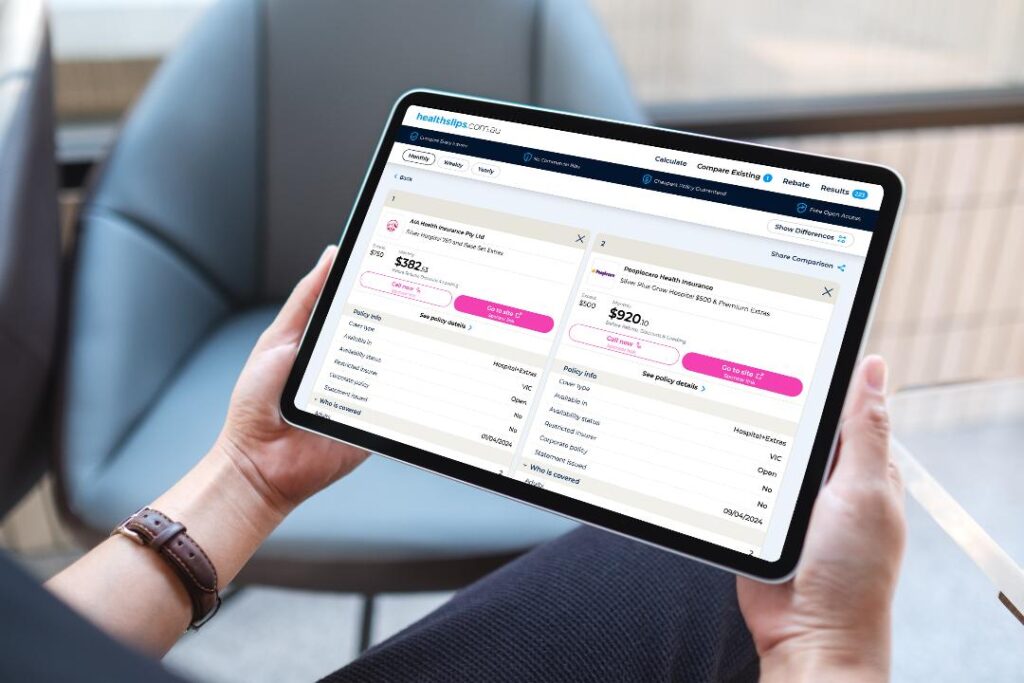

Once you’ve got a good picture of your budget and health needs, it’s time to search for the right policy. At healthslips.com.au, you can compare every policy from all 48 health insurance providers to find the best value cover, without having to enter any contact details. There’s a massive variation in premium prices – look at how much you could save by using our Calculator to change policies:

COUPLES POLICY PRICE COMPARISON

Combined Hospital and Extras Cover in VIC, excess up to $750, including open and restricted insurers

| Tier | Cheapest monthly | Expensive monthly | Difference monthly | Difference annually |

| Basic | $239.60 | $568.44 | $328.84 | $3,946.08 |

| Bronze | $301.15 | $596.20 | $295.05 | $3,540.60 |

| Silver | $382.53 | $920.10 | $537.57 | $6,450.84 |

| Gold | $560.84 | $1,409.53 | $848.69 | $10,184.28 |

Calculations completed 4 March 2025 at healthslips.com.au.

Basic: 64 policies from 23 insurers including 18 open insurers and 5 restricted insurers.

Bronze: 87 policies from 17 insurers including 12 open insurers and 5 restricted insurers.

Silver: 152 policies from 18 insurers including 16 open insurers and 2 restricted insurers.

Gold: 68 policies from 17 insurers including 8 open insurers and 9 restricted insurers.

Compare your health insurance policy with others on the market, or find a new policy.

Find out how much your premiums can be reduced the Government Rebate and Age-based Discount, if they apply to you.

See how easy it is to change insurers and remember you won’t have to serve any waiting periods again if you’re staying at the same level of cover.

With the healthslips.com.au Calculator, you can compare your existing policy against policies for singles, couples or for your entire household (including the kids). You can also compare different levels of cover, such as Gold vs Silver Hospital Cover. It’s the simplest, most accurate way to make a true comparison of health insurance policies out there and find the best fit for you, at the best price.

Trudie McConnochie

Writer and Researcher

Knowledge is power – that’s the guiding principle behind everything Trudie writes, and it’s a philosophy she brings to her work at healthslips.com.au. By breaking down complex information into easy-to-understand blogs and stories, she aims to empower Australians to make the best choices and an informed decision around private health insurance.

Trudie understands firsthand some of the complexity of private health insurance having moved to Australia from New Zealand and having to navigate a vastly different public healthcare system and health insurance structure.

Trudie holds a Bachelor of Communication Studies (journalism major) from the Auckland University of Technology.